The Utah based Chenoa fund homebuyer program offers a forgivable soft second grant option. The Chenoa Fund forgivable soft second grant program also allows for 3.5% or 5% of the purchase price to be used towards your down payment on an FHA first mortgage loan. The forgivable soft second will be treated and recorded as a second mortgage with no interest or monthly payments. If you keep your home and make on time payments for a minimum of three years the Soft Second will be forgiven.

Qualification & Highlights:*

Purchase loans only

Must qualify for an FHA loan

3.5% of purchase price available for down payment

May be used anywhere in Utah

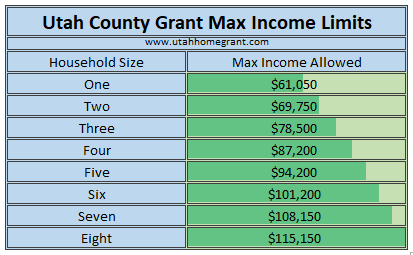

Must follow maximum income limits

Owner occupied only

1-2 Unit property (additional restrictions apply)

Min Fico Score 600

Utah County has a first time buyer program that will allow up to $40,000 in down payment assistance (DPA). The ‘Loan to Own’ down payment assistance program is available in all cities in Utah County except for Eagle Mountain, Fairfield, Alpine and Provo. The DPA can be used for down payment and closing costs, but no prepaid items such as interest, taxes and insurance. The final amount of the DPA will be determined by the type of mortgage you get and the home buyers closing costs. If you plan to sell the home within two years of closing this is not the assistance for you. If you do sell within two years of closing you may face a hefty $5,000 penalty in addition to paying the full amount of the DPA given to you back. If selling in within two years is a possibility you may want to consider either the Chenoa Fund or a Utah Housing loan.

Qualifications & Requirements:

Min of 650 qualifying fico score

Must be at least six months with current employer

Maximum purchase price of $551,000

First time home buyer only

Must be under maximum income limits

$5,000 penalty if property sold within two years of closing

0% Interest no payments as long as you live in the home

DPA must be paid back in full when the property is no longer the primary residence of the borrower(s)

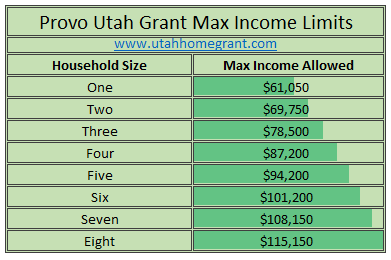

Provo City, Utah has a first time homebuyer program that offers up to $40,000 in an effort to revitalize communities in Provo. Home Purchase Plus is a down payment assistance program that was recently introduced to help all of Provo City increase the amount of new and first time homebuyers. The Community Development Block Grant (CDBG) is a federally funded program and is administered through the US Department of Housing and Urban Development (HUD) and is responsible for this allocation of funds.

The total amount of grant (up to $40,000) is determined by the mortgage programs minimum required down payment plus up to 5% in closing costs depending on the type of mortgage acquired.

As long as you own and occupy the home, the $40,000 first time homebuyer program is an interest free (0%) no payment loan.

Qualifications & Requirements for Grant:

You must be able to put down $1,000 of your own money

Home must be located within Provo, Utah

Must be a first time homebuyer (no ownership in a principal residence in the last 3 years)

Must meet income eligibility and be at current job for at least 6 months

Applicants must take “Pre-Home-Ownership Counseling” offered through Community Action or NeighborhoodWorks Provo

Purchase price cannot exceed $551,000

Property may be a single-family home, one half of a twin home, a condominium or town home, no renter displacement

Can not have own assets of more than $15,000

If home is sold or vacated within two years a $5,000 pre-payment penalty will be applied

The Utah based Chenoa Fund home buyer program offers a Repayable Second mortgage for anyone who qualifies and is over the income limits for the area. Saving money can be hard even if you are making above the median income, however you can still get help with your down payment. The Chenoa fund program will help you with a repayable second mortgage of 3.5% of the purchase price to help with the down payment of your FHA loan. This home buyer program will require the homebuyer to make payments and payoff the amount borrowed for the down payment. Only when the assistance is paid in full will the lien be removed from title.

The Utah based Chenoa Fund Grant is the favorite program available for most Utah home buyers. With this grant it does not matter if you are a first time buyer or have owned a home before. The grant will be completely forgiven shortly after closing. You are virtually receiving instant equity in your home. All programs with the Chenoa Fund Grant will require a homebuyer to qualify for an FHA first mortgage. When a home buyer is ready for closing they are able to receive 3.5% grant/gift of the purchase price of the home they are purchasing. Typically this will cover your entire down payment for the home. There are no geographical restriction so the grant is available for the entire state of Utah.

The Chenoa Fund is an affordable housing program that provides a down payment solution in conjunction with FHA loans. It fulfills a need for qualified homebuyers that do not have or do not want to use their own funds for a down payment. There are three different programs available to fit most homebuyer’s unique needs. The three programs are Grant/Gift, Forgivable Soft Second & the Repayable Second.

The Utah Housing HomeAgain Loan can be used by first time homebuyers or buyers that have previously owned a home. It allows for 2+ units as long as one is owner occupied. It is a great mortgage for anyone who does not have or does not want to put an initial down payment on a home. The DPA portion allows for up to 6% of the FHA first mortgage loan in the form of a fixed rate second lien to go towards down payment and/or closing costs.

Qualification and Requirements:*

Must qualify for an FHA loan

Minimum of 620 mid Fico score

Purchase loans only

6% of the first loan amount is available for DPA

May be used anywhere in Utah

Maximum qualifying income limit $151,900

No maximum purchase price

The Utah Housing Freddie Mac HFA Loan is not just a first time homebuyers program. This Utah down payment assistance (DPA) program allows for first time buyers and previous homeowners. It is also the only conventional Freddie Mac program they offer currently. To qualify you must have a minimum of a 700 fico score and be able to qualify for a conventional mortgage. The DPA is 6% (up to $25,000) of the first mortgage amount and can be used for down payment and/or closing costs. The property must be owner occupied and throughout the term of the UHC loan no portion of the property may be rented.

Qualification and Requirements:*

Purchase loans only

6% (up to $25,000) of the first loan amount is available for DPA

May be used anywhere in Utah

Maximum income limits $134,100

Debt ratio will be limited to a maximum of 50%

Homebuyer Education required

Single family units only

The Utah Housing Corporation offers several options for down payment assistance programs for first time buyers and buyers who have previously owned a home. Utah legislation created the Utah Housing Corporation (UHC) in 1975 to serve the public to provide an adequate supply of money with mortgage loans at a reasonable interest rate. This Utah mortgage homebuyer program is very helpful with low to moderate income families.

Since the UHC was created it has grown to offer five different types of programs. Each program has its unique advantages and helps Utah home ownership grow. You can explore each loan by clicking the link below.

The Utah Housing First Time Buyer Program called FirstHome Loan is a great program for any first time buyer. The Utah housing First Time Buyer Program allows for up to 6% of the first mortgage loan as down payment assistance (DPA). This DPA is in the form of a 30 year fixed rate second loan. The DPA can be used for down payment and/or closing costs for the FHA first mortgage. You must be a first time buyer and be able to qualify for an FHA mortgage.

Qualification and Requirements:*

Must qualify for an FHA loan

No Portion of the property may be rented throughout the term of the UHC Loan

6% of the first loan amount is available for DPA

Minimum of 660 Fico score

No geographical restriction in Utah

See below for income and max purchase price

Income and Purchase Price Limits for Utah Housing Loans