The Utah Housing Score Loan is Utah mortgage loan program for borrowers who do not meet the minimum Fico requirement of the FirstHome or HomeAgain loan. For the Score Loan Utah Housing Corporation has set a 620 mid score for the minimum fico score. You still must be able to qualify and meet all the requirements for an FHA backed mortgage. The DPA portion allows for up to 4% of the FHA first mortgage loan in the form of a fixed rate second lien and can go towards down payment and/or closing costs. The property must be owner occupied and throughout the term of the UHC loan no portion of the property may be rented.

Qualification and Requirements:*

- Must qualify for an FHA loan

- Minimum of 620 mid Fico score

- Purchase loans only

- 4% of the first loan amount is available for DPA

- May be used anywhere in Utah

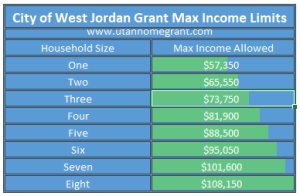

- Must follow maximum income limits

- Debt ratio will be limited to a maximum of 45%

- Homebuyer Education required within 90 days of closing

- Maximum income limit is $95,800

- No maximum purchase price

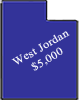

The City of West Jordan, Utah is providing up to $10,000 for first time homebuyers that purchase a home within West Jordan City limits. This grant may be applied to half of the required down payment and/or one-time closing costs. Funds are distributed on a first-come, first-serve basis. The home buyer must occupy the home for at least five (5) years following the purchase, any change in ownership or occupancy will require repayment of the grant funds. After five (5) years the grant is forgiven in full. If the home is sold or ceases to be occupied by the home buyer within the first five (5) years the lien is forgiven at a rate of 20% per completed year and the balance remaining will be due in full to the City.

Qualifications & Requirements:

- Home buyer must contribute a minimum of $2,500 cash out-of-pocket towards the purchase, these funds may NOT be gift funds

- Applicant must meet income qualifications and cannot have owned a home within the last 24 months

- Co-signers are not allowed

- Existing, new construction single-family homes, condos, and townhomes are permitted

- Housing debt cannot exceed 35% of the household monthly income and total debt cannot exceed 45% of the household monthly income

- Home must be owner occupied

- Applicant must attend and receive a completion certificate from a HUD approved homebuyers education class

- Visual inspection completed by the City for any safety or health concerns