The Utah based Chenoa Fund Grant is the favorite program available for most Utah home buyers. With this grant it does not matter if you are a first time buyer or have owned a home before. The grant will be completely forgiven shortly after closing. You are virtually receiving instant equity in your home. All programs with the Chenoa Fund Grant will require a homebuyer to qualify for an FHA first mortgage. When a home buyer is ready for closing they are able to receive 3.5% grant/gift of the purchase price of the home they are purchasing. Typically this will cover your entire down payment for the home. There are no geographical restriction so the grant is available for the entire state of Utah.

The Chenoa Fund is an affordable housing program that provides a down payment solution in conjunction with FHA loans. It fulfills a need for qualified homebuyers that do not have or do not want to use their own funds for a down payment. There are three different programs available to fit most homebuyer’s unique needs. The three programs are Grant/Gift, Forgivable Soft Second & the Repayable Second.

The Utah Housing HomeAgain Loan can be used by first time homebuyers or buyers that have previously owned a home. It allows for 2+ units as long as one is owner occupied. It is a great mortgage for anyone who does not have or does not want to put an initial down payment on a home. The DPA portion allows for up to 6% of the FHA first mortgage loan in the form of a fixed rate second lien to go towards down payment and/or closing costs.

Qualification and Requirements:*

Must qualify for an FHA loan

Minimum of 620 mid Fico score

Purchase loans only

6% of the first loan amount is available for DPA

May be used anywhere in Utah

Maximum qualifying income limit $151,900

No maximum purchase price

The Utah Housing Score Loan is Utah mortgage loan program for borrowers who do not meet the minimum Fico requirement of the FirstHome or HomeAgain loan. For the Score Loan Utah Housing Corporation has set a 620 mid score for the minimum fico score. You still must be able to qualify and meet all the requirements for an FHA backed mortgage. The DPA portion allows for up to 4% of the FHA first mortgage loan in the form of a fixed rate second lien and can go towards down payment and/or closing costs. The property must be owner occupied and throughout the term of the UHC loan no portion of the property may be rented.

Qualification and Requirements:*

Must qualify for an FHA loan

Minimum of 620 mid Fico score

Purchase loans only

4% of the first loan amount is available for DPA

May be used anywhere in Utah

Must follow maximum income limits

Debt ratio will be limited to a maximum of 45%

Homebuyer Education required within 90 days of closing

Maximum income limit is $95,800

No maximum purchase price

The Utah Housing Freddie Mac HFA Loan is not just a first time homebuyers program. This Utah down payment assistance (DPA) program allows for first time buyers and previous homeowners. It is also the only conventional Freddie Mac program they offer currently. To qualify you must have a minimum of a 700 fico score and be able to qualify for a conventional mortgage. The DPA is 6% (up to $25,000) of the first mortgage amount and can be used for down payment and/or closing costs. The property must be owner occupied and throughout the term of the UHC loan no portion of the property may be rented.

Qualification and Requirements:*

Purchase loans only

6% (up to $25,000) of the first loan amount is available for DPA

May be used anywhere in Utah

Maximum income limits $134,100

Debt ratio will be limited to a maximum of 50%

Homebuyer Education required

Single family units only

The Utah Housing Corporation offers several options for down payment assistance programs for first time buyers and buyers who have previously owned a home. Utah legislation created the Utah Housing Corporation (UHC) in 1975 to serve the public to provide an adequate supply of money with mortgage loans at a reasonable interest rate. This Utah mortgage homebuyer program is very helpful with low to moderate income families.

Since the UHC was created it has grown to offer five different types of programs. Each program has its unique advantages and helps Utah home ownership grow. You can explore each loan by clicking the link below.

The Utah Housing First Time Buyer Program called FirstHome Loan is a great program for any first time buyer. The Utah housing First Time Buyer Program allows for up to 6% of the first mortgage loan as down payment assistance (DPA). This DPA is in the form of a 30 year fixed rate second loan. The DPA can be used for down payment and/or closing costs for the FHA first mortgage. You must be a first time buyer and be able to qualify for an FHA mortgage.

Qualification and Requirements:*

Must qualify for an FHA loan

No Portion of the property may be rented throughout the term of the UHC Loan

6% of the first loan amount is available for DPA

Minimum of 660 Fico score

No geographical restriction in Utah

See below for income and max purchase price

Income and Purchase Price Limits for Utah Housing Loans

Duchesne, Garfield, Iron, Kane, Piute, San Juan, Sanpete, Wayne

$130,200

$151,900

$513,200

FirstHome

Juab, Utah

$130,800

$152,600

$613,400

FirstHome

Salt Lake

$113,800

$130,850

$635,600

FirstHome

Tooele

$113,800

$130,850

$635,600

FirstHome

Washington

$109,900

$126,800

$608,500

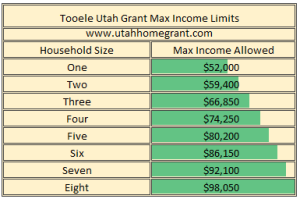

The Tooele County Housing Authority (TCHA) helps qualified first time home buyers purchase a home by providing a federally funded loan of up to $10,000 to assist with down payment and/or closing costs. Loans are dispersed on a first come, first serve basis and can be applied to the purchase of a single-family home, condo, cooperative unit, or combination of manufactured housing and lot.

Qualifications & Requirements:

No homeownership in the last three (3) years

Applicant must contribute $1,000 of own money

Applicant must attend a Housing and Urban Development (HUD) approved homebuyer education class and provide a certificate of completion

A home inspection completed by a Utah licensed home inspector for health and safety concerns and lead-based paint for homes built prior to 1978

Home must be located in Tooele County

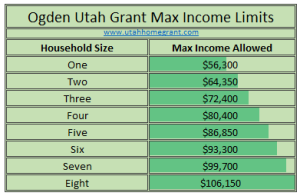

The “Own in Ogden” first time homebuyer program has helped hundreds and hundreds of people realize their dream of owning a home in Ogden. This government grant program offers $10,000 to first time buyers, $15,000 to state certified K-12 classroom teachers and $20,000 to sworn Police Officers and Firefighters when purchasing a home in Ogden city. These are zero interest, no monthly payment, down payment assistance grants. These grant funds are issued to first time home buyers as a loan attached to the property which will become due in full if the borrower ceases to occupy the property, sells the property or defaults on any of the established terms upon receiving the grant funds.

Qualifications & Restrictions for “Own in Ogden”:

Property must be zoned residential

Buyer must contribute $500 of own money towards purchase and take fee simple title to property

First time homebuyer grant funds may be used for down payment, closing costs or principal reduction towards the first mortgage loan balance

Property must meet minimum safety, construction, and habitability with no unresolved code enforcement violations

Buyers assets in excess of $20,000 must be applied towards the home purchase

Buyers must purchase property within the eligibility area of Ogden city

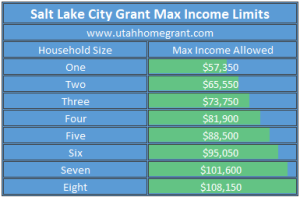

If yu are a Utah first time homebuyer looking for a home in Salt Lake City, a $39,000 neighborhood down payment assistance grant is available. The “Own in Salt Lake City” program is a federally funded, deferred loan/grant program. This program assists eligible first time homebuyers purchase single family homes with a deferred loan/grant up to $39,000. If you are purchasing outside of Salt Lake City you may qualify for the Salt Lake County First Time Buyer Program.

Qualifications & Requirements for Salt Lake City Home Grant:

• Must purchase within Salt Lake City boundaries • Actual grant amount will be determined on the funds needed to close determined by the loan applicant qualifies for. Receiving the maximum grant amount is not guaranteed. • Deferred loan funds shall be repaid by the recipient in full if the homeowner sells; exchanges or transfers title; refinances for any other reason than to lower interest rate; or ceases to occupy to property as primary residence before the forgiveness term is satisfied.

• Purchase price cannot exceed $522,500 • Must be a first time homebuyer (no home ownership in the last three years) • Visual assessment must be completed • Applicant must complete a homebuyer education course and pre-purchasing counseling • Must be below maximum income limits